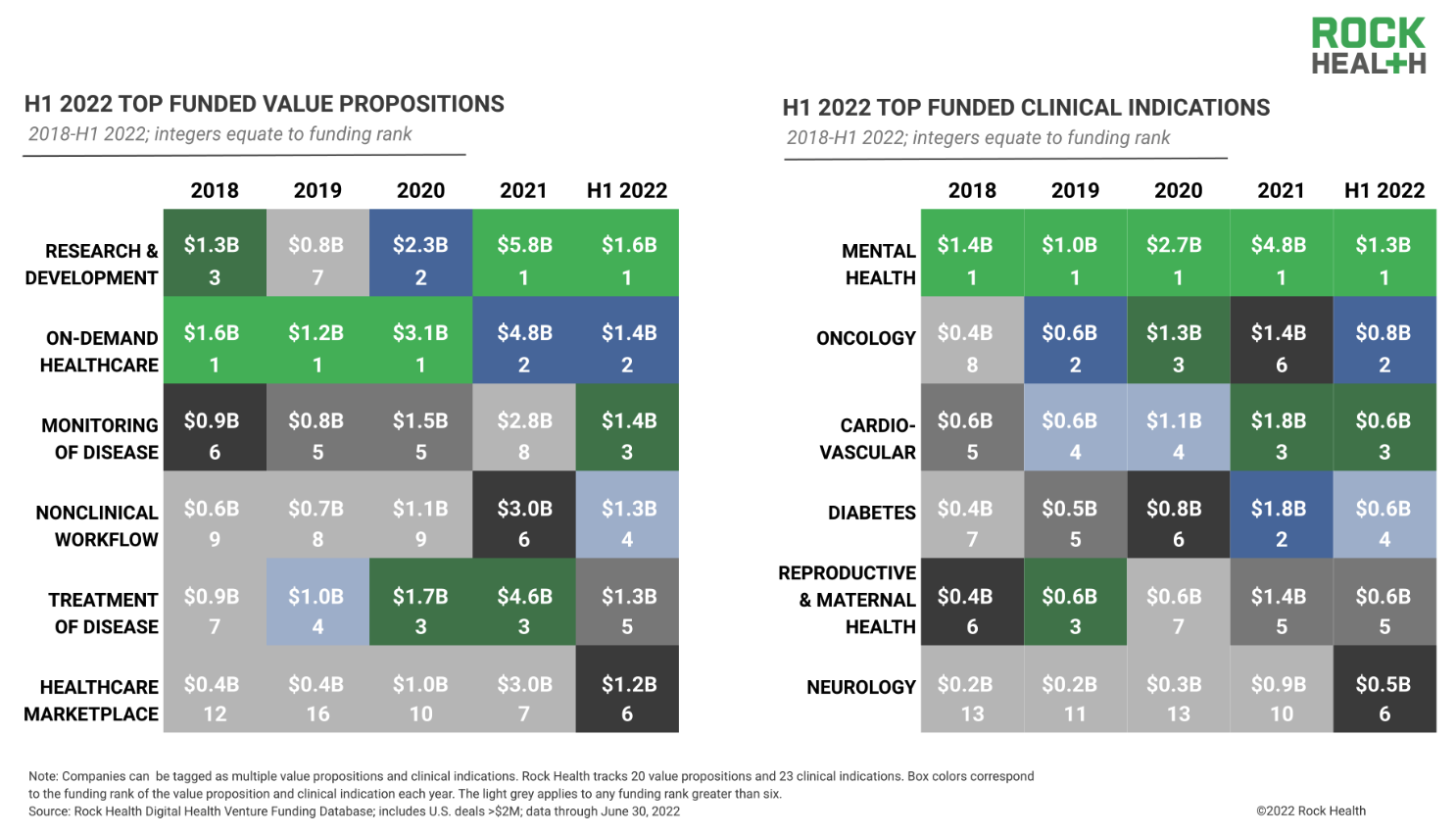

Mental health continued to top all digital health investment in 2022’s first half.

Yet the entire market may be headed for a potential cooldown, with inflation, global unrest and regulatory uncertainty contributing to more conservative mindsets among investors and founders alike.

“Coming off the launch ramp of 2021, digital health founders, funders and corporate execs were anxious to see the sector’s 2022 trajectory,” venture capital and advisory firm Rock Health wrote in a new report. “The first quarter of this year signaled the beginnings of a market cooldown and spurred inquiries regarding frothiness in digital health funding.”

Mental health easily outpaced all other sub-sectors in 2021, with companies in the space collectively raising $4.8 billion – just $300 million off the previous three years combined.

In comparison, mental health companies hauled in $1.3 billion in the first two quarters of 2022. Nearly all of that investment – about $1 billion – came in the year’s first three months, which may signal “a slowdown in funder excitement,” according to Rock Health.

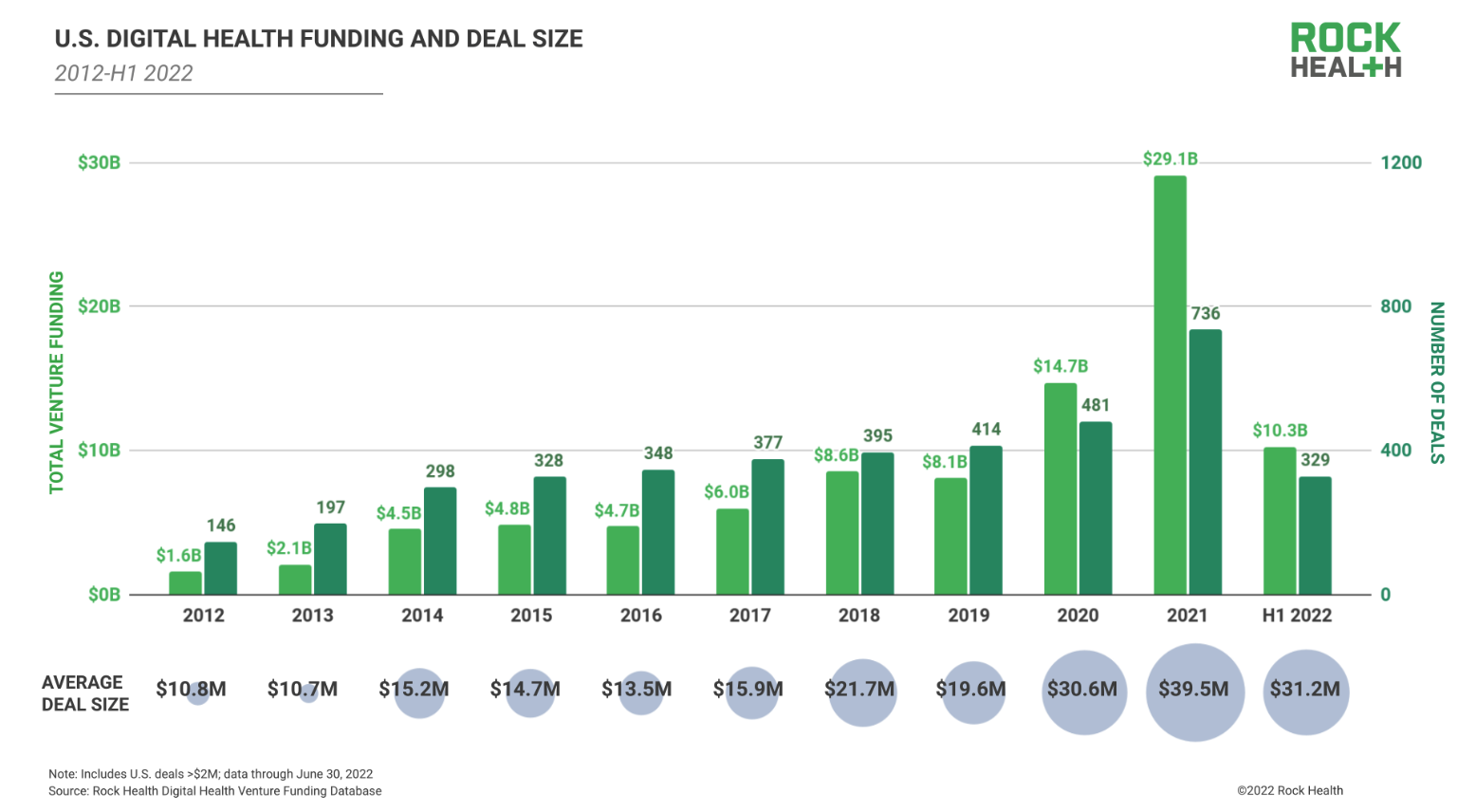

Overall, digital health investment reached $10.3 billion in the first half of 2022. The full year’s projected funding estimate is about $21 billion. Although that’s markedly less than 2021’s total of $29.1 billion, it’s still substantially above 2020 and 2019 levels, when investors pumped $14.7 billion and $8.1 billion into digital health, respectively.

“This multi-year trend indicates continued funding growth, with funding in 2021 perhaps standing out as an anomaly,” Rock Health explained in its report.

Of the $1.3 billion in mental health investment in 2022’s first half, nearly one-fifth of the total came from a single funding round: Lyra Health’s $235 million Series F, led by Dragoneer, with participation from Salesforce Ventures and existing investor Coatue Management.

Noteworthy examples of mental health investment in Q2 include SpectrumAi’s $9 million seed round, led by F-Prime Capital and Frist Cressey Ventures. Public benefit corporation Osmind Inc. additionally announced a $40 million Series B round in May, led by DFJ Growth.

While 2022 investment is on track to finish far below 2021’s total in terms of value, the digital health market isn’t too far behind last year from a volume standpoint.

So far, there have been at least 329 digital health funding deals in 2022, which translates to about 658 over a 12-month period. Overall, there were 738 digital health funding deals in 2021.

The average deal size in H1 2022 was $31.2 million, with most activity coming from repeat investors, according to Rock Health. Generally, repeat investors familiar with the digital health space and long-term demand are less likely to be scared away by temporary external factors, the firm noted.

Ships passing in the night

Some digital health darlings have already begun to prepare for an investment cooldown, at least compared to 2021 standards, by laying off workers to extend their cash runways.

“[Investor] confidence in both public and private markets was shaken by global conflict and inflation concerns,” Rock Health explained in its report. “Notable investors Y Combinator and Sequoia Capital published letters to their portfolio companies warning them to prepare for an economic downturn, and venture funds in general battened down their hatches.”

On Monday, technology-enabled primary care company Forward Health revealed that it’s trimming 5% of its workforce. Ro, the digital health company that hit a $7 billion valuation in February, moved to slash 18% of its workforce in June.

In the mental health sub-sector, Cerebral previously disclosed plans to implement layoffs starting in July. Cerebral CEO Dr. David Mou described the layoffs as part of a company-wide refocusing on its core services.

“We’re going to deprioritize some of these more exploratory and peripheral service lines that we were considering,” Mou told Behavioral Health Business. “We were looking at primary care beforehand. That’s on pause for now. So efforts such as that, like international expansion, we’re going to put that on pause, but let’s really focus on getting mental health right.”

The dip in digital health investment has impacted M&A activity and public exits as well.

Last year, digital health averaged 23 exits via merger or acquisition each month, according to Rock Health. Meanwhile, Q2 2022 averaged 13 exits per month, while Q1 averaged 20.

What’s more, after nearly two dozen public-market exits in 2021, there have been zero in 2022.

In part, the decrease in M&A activity is due to buyers taking a more measured approach amid economic turbulence. Some buyers may likewise be concerned about increased oversight of digital health companies from government agencies, a trend that’s especially evident in the mental health arena.

At the same time, there’s beginning to be a clear “mismatch” of perceived valuations between sellers and buyers.

“There’s just ships passing in the night that could be matched, but won’t be matched,” Michael Yang, managing partner at OMERS Ventures, previously told BHB.

Companies featured in this article:

Cerebral, lyra health, OMERS, Osmind, Rock Health, SpectrumAi