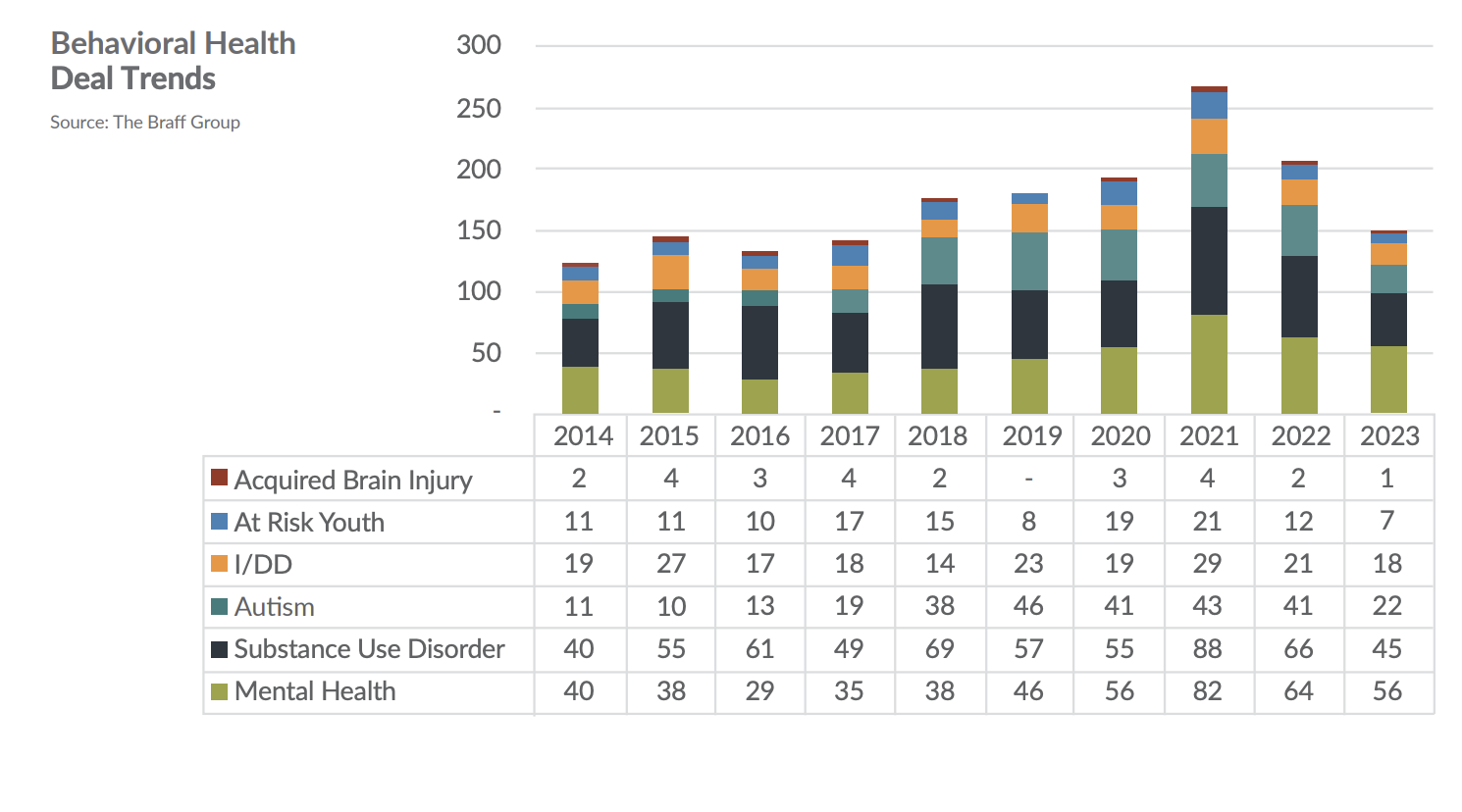

While behavioral health dealmaking remained soft in 2023, one sector completed a record number of deals last year.

Seventeen deals were completed in the outpatient partial hospitalization program (PHP), intensive outpatient program (IOP) and counseling sectors.

Outpatient SUD treatment has become more popular because it is more affordable for patients and payers and easier for operators to scale.

“Every other segment is in a significant downswing,” Dexter Braff, president of The Braff Group, said at Behavioral Health Business’s VALUE conference. “It will be interesting to see if we see that again this year. We should, because that’s where the activity and interest from payers is at.”

Overall, behavioral health M&A has been in a relative slump for 18 months, according to a new report from The Braff Group. Although each quarter of 2023 was consistently slow, this cannot be attributed to a lack of interest in the marketplace.

“The patterns over the last 10 years have been driven much more by macroeconomic trends than by individual microtrends within the healthcare services arena,” Braff said.

Higher interest rates, inflation, staffing shortages, and unrest in Eastern Europe and the Middle East are macroeconomic factors impacting dealmaking across industry segments.

Segment breakdown

Mental health deal flow still managed to outpace SUD deals with 11 more deals completed. Outpatient transactions were popular in this segment as well as in SUD treatment.

“It’s one of the few areas that is still in what we call the positive zone,” Braff said.

Recent declines in mental health M&A may be attributed to macroeconomic factors, but another mechanism may also be at play. The behavioral health industry has repeatedly been called “fragmented,” and many providers have only one or two offices. Opportunities for more significant mental health deals involving multi-office providers may run out as the pool of viable acquisition candidates shrinks.

Buyers are also experiencing anxiety regarding severe mental illness due to concerns with liability and the potential difficulty of patients. The segment has higher margins, greater barriers to entry and limited competition, however, creating substantial opportunity for dealmaking.

One notable exception to this trend is digital behavioral health provider Lyra, which recently introduced a multipronged offering for individuals with complex mental health issues.

“For those of you who like to zig when the market zags, severe mental illness is an open window right now,” Braff said.

Approximately 21.5 million American adults have co-occurring mental illnesses and substance use disorders, according to SAMHSA’s most recent National Survey on Drug Use and Health. However, 2023 saw little cross-segment activity.

“It’s extremely difficult to overcome the barriers to merge services across the various different segments when you do that through acquisition,” Braff said.

Cross-segment deals require overcoming a “silo mentality,” Braff said. They are also less popular among private equity, which accounted for more than 60% of all behavioral health deal flow since 2018. PE firms prefer narrow segments of business, and largely do not make cross-segment deals because they involve too much time and risk.

“[Cross-segment deals] are largely better suited for folks who are building these models from the ground up,” Braff said.

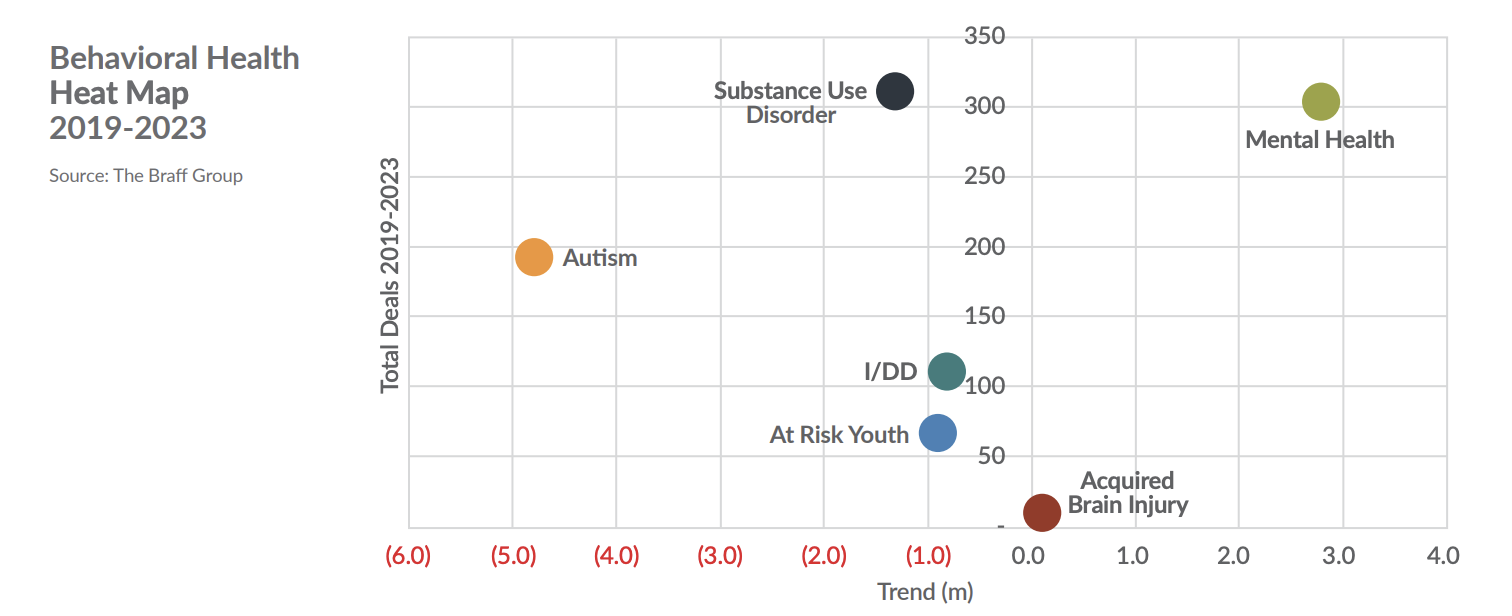

While dealmaking in the intellectual and developmental disability (IDD) space has remained flat “but not that bad,” autism deals have trended down significantly after their peak in 2019.

“It’s eased up over the last couple of years, mostly on some failed consolidation strategies,” Braff said. “[There has been] some real focus on reimbursement. And when there’s focus on reimbursement, that’s generally not a good thing.”

Behavioral health M&A outlook

The outlook on 2024 behavioral health M&A is “fairly favorable,” with multiple factors that have plagued the industry in recent years set to ease up.

Inflation has slowed down, there has been a “soft landing” after the COVID-19 pandemic, and staffing issues, while persistent, have improved. The Federal Reserve System has also signaled that the first in a series of rate cuts will occur in the next couple of months.

Additionally, new telehealth guidelines have made digital behavioral health more accessible, and the gap in value expectations is narrowing.

Despite favorable projections for 2024, there is still cause for concern. More states may be developing notification requirements, which could make the process of closing a deal take longer.

Currently, 13 states have regulation that requires notification before a health care transaction can be completed. The Braff Group suspects that many states are developing such policies.

“From a seller’s perspective, nothing good happens between the signing of a letter intent and closing,” Braff said. “If your revenues go up, the buyers don’t raise the purchase price. But if something bad happens, they lower it or they leave.”