The Center for Autism and Related Disorders’ (CARD) bankruptcy doesn’t foreshadow a new level of doom and gloom for the industry as a whole.

Although CARD is one of the largest companies operating in the space, it shouldn’t be used as a bellwether for autism therapy’s future outlook, several insiders told Behavioral Health Business.

“I’d say the CARD transaction is more indicative of where we are in the market than it is of where the market is going,” Robert Aprill, managing director at the M&A firm Physician Growth Partners, told BHB.

Headwinds common to autism therapy were the driving force behind CARD’s Chapter 11 bankruptcy, court documents state. But CARD is an isolated example of a behavioral health company needing a court-ordered restructuring due to “razor-thin liquidity.”

If anything, CARD filing for Chapter 11 solidifies several industry trends already underway. Stagnant fee-for-service reimbursement rates, along with rising inflation and interest rates, have strained the autism sector.

In turn, some operators have made painful business adjustments, including job cuts. Others that were once in hyper-growth mode and active on the M&A front pivoted to more slow-and-steady approaches to expansion and focusing on organic growth.

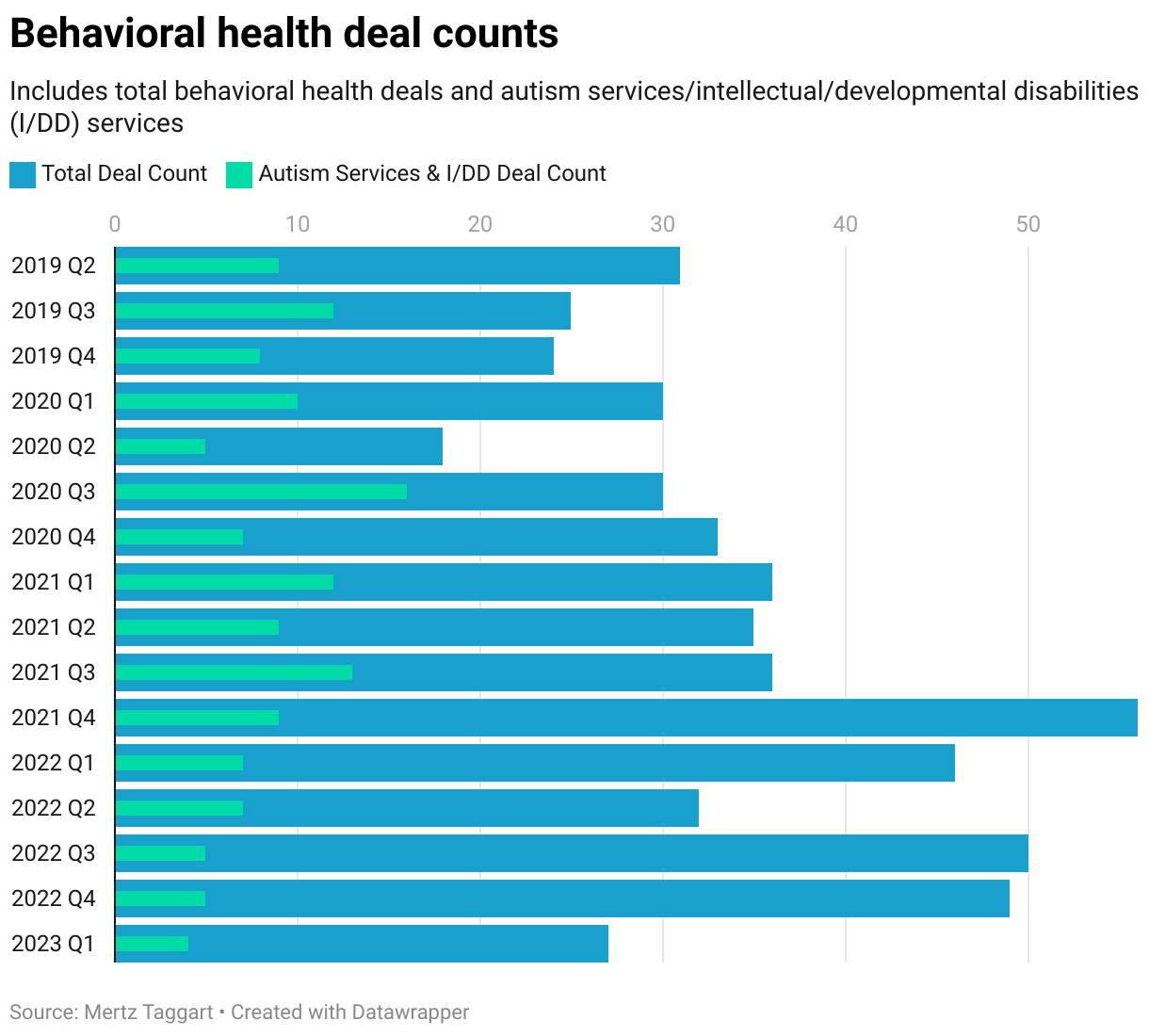

That has translated to deal volumes being down during 2023’s first quarter.

Kevin Taggart, managing partner and co-founder at M&A advisory firm Mertz Taggart, told BHB he expects this trend to continue in the second quarter, with transaction levels picking up next year.

“There’s always a market for good companies here and there,” he said.

Autism therapy demand outweighs challenges

As part of the CARD’s bankruptcy, majority shareholder Blackstone Inc. (NYSE: BX) agreed to sell its stake to Doreen Granpeesheh, the company’s founder and former CEO, for $25 million. Sangam Pant is also involved with the bid.

CARD was valued at $700 million in 2018, when Blackstone acquired a 70% stake in the company.

Despite the current headwinds that CARD and its peers are navigating, interest in meeting the staggering demand for autism services overrides concerns about the segment.

As many as 1 in 36 children in the U.S. have autism, up from the previous estimate of 1 in 44. In comparison, the estimated autism rate in the U.S. was one in 150 in 2000

The growing rate of autism has also come with commensurate increases in expectations for people with autism to succeed in life. Understanding of the condition and related therapies has improved, with more accessibility as well.

All of this means continued, near-unrelenting demand for services, Matt Bogenschutz, associate professor at the School of Social Work at Virginia Commonwealth University, told BHB.

“If there is a chilling effect [to CARD], it’ll be very temporary, and hopefully then people will take a more sober view and realize that there is a great need in the space,” Bogenschutz said. “While I think the provision of any human service is never going to be a huge moneymaker, I do think there’s still space for investments.”

An isolated impact

CARD was among a cohort of autism therapy providers that took advantage of a frothy investment and M&A market. In hindsight, it did so at a time when investors and operators lacked the degree of savvy now recognized as needed when considering the proposition of growing and operating national autism therapy companies.

Critics of CARD, or of the involvement of private equity investment in the space more broadly, point to the influence of large investors as a negative. Some will possibly make the case that CARD’s fate is indicative of where other companies may be heading.

“I would respectfully disagree that this is the writing on the wall for anyone that’s sought out private equity backing,” Mike Moran, co-founder and executive advisor of M&A Healthcare Advisors, told BHB. “I don’t think this is a bigger indication of what’s to come at all.”

CARD is something of a one-of-one case, Moran said, noting that bankruptcy is indicative of what happens when any company runs into trouble with overhead and generating cash flow.

As of April 2023, the company’s annual earnings before interest, taxes, depreciation and amortization (EBITDA) were a $22 million loss. Its net loss totaled $82 million, while revenue totaled about $160 million for the same period, according to court documents.

James Cassel, chairman and co-founder of the investment bank Cassel Salpeter & Co., also doesn’t expect a wider negative impact from the CARD bankruptcy sale. It does reflect a change in the state of the market for buying and selling autism therapy companies, he told BHB.

“What this is doing is resetting values,” Cassel said, pointing to elevated multiples around the time CARD sold. “I don’t think the old valuations are going to stand. … The market’s just a little quieter.”

Data from M&A firm The Braff Group shows that multiples for autism therapy companies have compressed in recent years. Multiples ranged from 5.75 times earnings to 14 times earnings from the middle of 2016 to the middle of 2019.

Between 2020 and 2023, high-end multiples tumbled while low-end multiples only ticked down slightly compared to the previous period. Those multiples stand at 5 to 10 times earnings, according to The Braff Group.

Peaks, valleys and centers

The Blackstone investment in CARD generated a great deal of excitement. It also lent a significant amount of legitimacy to the autism therapy space, Adam Abramowitz, managing director and head of health care at M&A and strategic advisory firm Intrepid Investment Bankers, told BHB.

"From an investment standpoint, there are clearly some peaks and valleys," Abramowitz said.

Echoing several other sources, Abramowitz expects investors to continue to strengthen their standards for what autism therapy companies will invest in. He called it a "heightening of discipline."

CARD’s struggles have also opened up the conversation about what care setting is best for autism providers. Court documents point to the company's leases for its treatment center as a major concern.

The industry has gravitated more towards center-based programs, Abramowitz said. There is a wide mix of home-based and center-based care in the autism therapy space.

The real estate needs for center-based care inherently add to an autism therapy provider's overhead. While home-based care is less efficient, it has become more accepted in the market after COVID, at least temporarily, closed centers.

Debt and market concentration

Like many other businesses, CARD's private equity backing came with a notable amount of debt. This likely became problematic since interest rates have skyrocketed since 2018.

The increased cost of debt slowed investment overall. Taggart suspects this also has the effect of inspiring greater scrutiny in dealmaking across behavioral health.

Over the last six months, he said, investors have lodged many more questions before submitting their offers.

"I don't know if that's being driven by lenders requiring more information, but that's my suspicion," Taggart said. "They're asking a lot more questions than they used to, say, a year ago — or certainly more than five years ago."

The CARD bankruptcy also demonstrates the inherent risk of leveraged buyouts like the one CARD underwent.

Court documents show CARD took on $235 million in debt on Nov. 21, 2018, as part of the deal with Blackstone. Its primary lender is New York-based Ares Capital Corp. That debt funded the company's expansion and development of its own electronic health record (EHR) system.

About $159.5 million of that debt remains.

One investment banking executive who spoke with BHB on background pointed out that while other autism therapy providers grew quickly across the country, CARD had a larger and more diffuse footprint.

As of February 2022, CARD offered services at 221 locations in 24 states. According to court documents, it had about 100 clinics in 2018. Today it lists 130 locations.

Rates from state Medicaid and state-focused private health plans make up 90% of the company's revenue, court documents show. Medicaid rates for autism services are low compared to other services. Also, rates for such therapies have remained flat on average in the U.S., acting effectively as cuts during inflation.

"I would assume that the average, blended rate per hour is substantially different [than other organizations]," the executive said. "CARD did not have as much cushion to absorb these impacts, maybe relative to other competitors that were more in lucrative markets or markets that have had higher reimbursements."

Companies featured in this article:

Blackstone, Center for Autism and Related Disorders, Intrepid Investment Bankers, M&A Healthcare Advisors, Mertz Taggart, Physician Growth Partners, Virginia Commonwealth University